Payment rails are the digital highways that transfer money between accounts. For any enterprise, selecting the optimal rail involves balancing transaction speed, operational costs, geographic reach, and end-user experience. Prominent examples include the Automated Clearing House (ACH) in the U.S. and the Single Euro Payments Area (SEPA) in Europe.

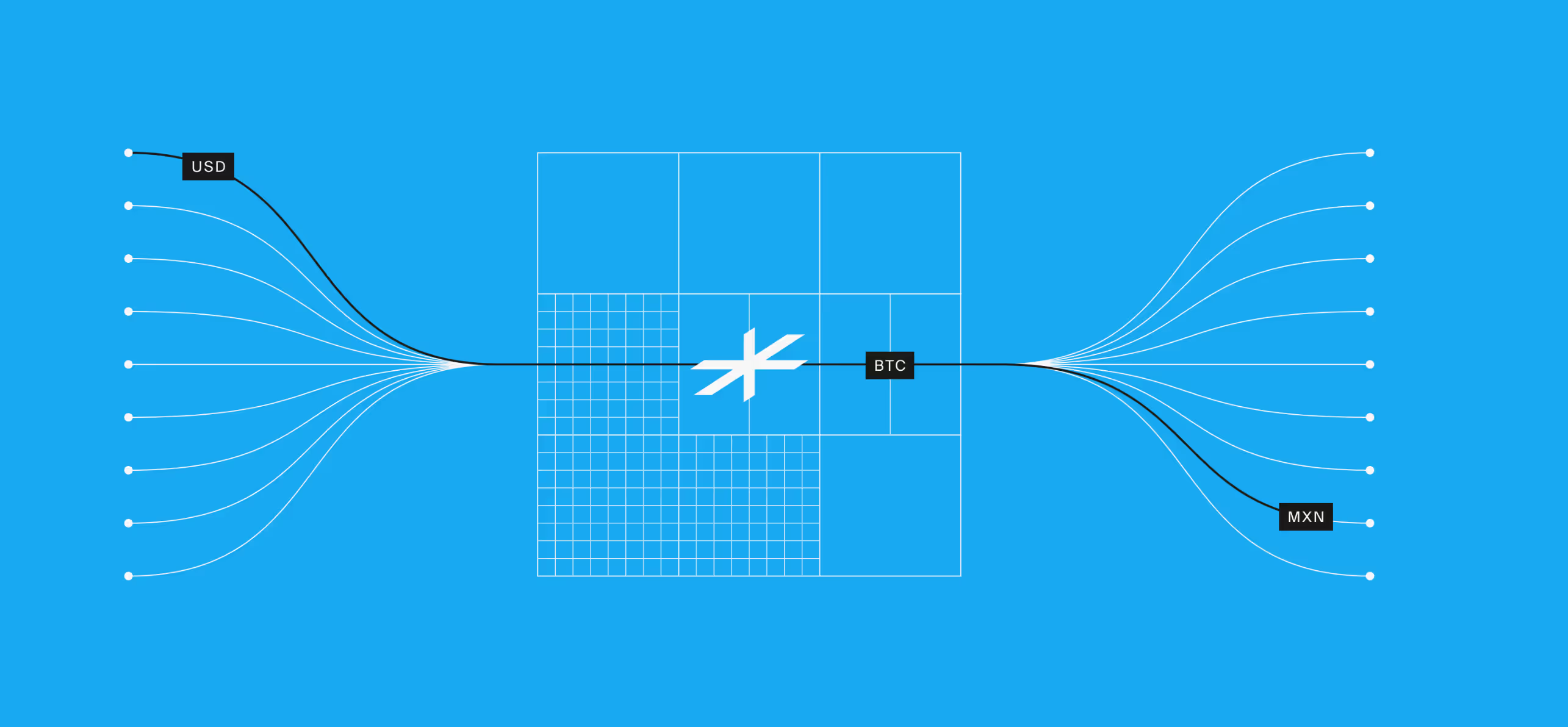

To address the limitations of these systems, Lightspark is pioneering a new category of payments infrastructure on Bitcoin’s open foundation, aiming to move money instantly and globally, much like information travels across the internet.

The Payment Rail Landscape

These networks are the backbone of the global economy, facilitating everything from payroll to international trade. Yet, many existing rails are a patchwork of slow, disconnected systems, resulting in settlement delays and high transaction fees for businesses and consumers.

Understanding ACH and SEPA

How ACH Works

The Automated Clearing House (ACH) is an electronic network for moving money between U.S. bank accounts, managed by Nacha. It functions as a financial hub, processing large volumes of credit and debit transactions. Using batch processing technology, ACH groups payments together and processes them at set intervals. A typical transaction starts when an originator initiates a payment. Their bank (ODFI) sends a batch of transactions to an ACH operator, like the Federal Reserve. The operator sorts the batch and forwards the transaction to the recipient's bank (RDFI), which then credits or debits the recipient's account, often on the same business day.

Strengths and Limitations of ACH

Strengths

- It is highly cost-effective, with transaction fees that are typically much lower than those for wire transfers or credit cards.

- The network is built for efficiency, processing billions of payments and enabling same-day settlement for most transactions.

- ACH is well-suited for recurring payments, making it ideal for subscriptions, payroll direct deposits, and automated bill payments.

Limitations

- The network is restricted to domestic U.S. transactions and cannot be used for international payments.

- Transactions are not instant and can take several days to fully settle, creating risk for businesses that deliver goods before payment is final.

- Financial institutions often impose daily transaction limits, which can be a constraint for businesses needing to move large sums of money.

How SEPA Works

The Single Euro Payments Area (SEPA) is a system designed to make cross-border euro (EUR) transfers as simple and cost-effective as domestic ones. Governed by EU regulations, it ensures payments between member countries cost no more than local transfers. The process begins when a sender initiates a EUR payment using the recipient's IBAN. The transfer is processed through standardized banking protocols and typically settles within one to two working days. This system facilitates seamless transactions across the Eurozone and other participating nations, generally without any receiving fees for the recipient.

Strengths and Limitations of SEPA

Strengths

- SEPA makes cross-border payments highly cost-effective, as transfers are often low-cost or free.

- The system is efficient, with standard transfers settling within one business day and an instant payment option available.

- It simplifies payments across Europe by covering all EU member states and several other participating countries.

Limitations

- The network is limited to euro-denominated transactions within its specific European member countries.

- Standard transfers are not instantaneous and can take several days to settle, introducing risk for businesses.

- Despite regulations, some banks may still find ways to charge extra fees for receiving SEPA payments.

ACH and SEPA Compared

Transaction Speed

ACH payments can take up to four days to settle, though same-day processing is available. SEPA transfers typically settle in one business day, with an instant option. In contrast, networks like Lightspark are built for instant, real-time money movement.

Fees

ACH transactions are cost-effective, typically costing businesses between $0.26 and $0.50. SEPA payments are also inexpensive, often being free or carrying minimal fees. Modern payment infrastructures like Lightspark aim to reduce these costs even further, promising payments at a fraction of today’s costs.

Cross-Border Capabilities

ACH is strictly for domestic U.S. transactions and cannot be used for international payments. SEPA facilitates cross-border transfers within 36 European countries. For truly global reach, platforms like Lightspark are designed to move money across borders to over 140 countries.

Security Protocols

ACH security is governed by Nacha operating rules, while SEPA relies on IBANs and signed mandates for authorization. Both are established systems, but modern networks like Lightspark add layers of security with built-in compliance and protocols designed for the digital age.

Operational Hours

Both ACH and SEPA are tied to traditional banking schedules, processing transactions primarily on business days. This contrasts with modern payment infrastructures like Lightspark, which are designed to be always on and enable 24/7 payments, regardless of holidays or weekends.

How ACH And SEPA Are Used

Payroll and Employee Salaries

ACH is ideal for paying U.S. employees, while SEPA handles payroll across the Eurozone. For global remote teams, Lightspark is superior, enabling instant, low-cost salary payments across 94+ countries in various currencies, bypassing the geographic and currency limitations of traditional rails.

Supplier and Vendor Payments

Businesses use ACH for domestic U.S. suppliers and SEPA for vendors within Europe. Lightspark accelerates this by enabling real-time, 24/7 payments, eliminating settlement delays. This allows companies to pay international suppliers instantly, unlocking new trade corridors without traditional banking friction.

Subscription Services and Recurring Bills

ACH and SEPA are effective for recurring debits like subscriptions within their regions. Lightspark’s Lightning Network excels at high-frequency micropayments, enabling flexible pay-as-you-go models. This offers instant settlement for services where traditional recurring payment models are too rigid or costly.

Cross-Border Payments for Digital Services

SEPA simplifies euro transfers within Europe, but ACH is not an option for cross-border payments. Lightspark offers a truly global network, allowing digital banks and exchanges to facilitate instant, low-cost international transfers in fiat or stablecoins, bypassing traditional banking delays and limitations.

Time for a New Standard

Unlike the slow, fragmented, and geographically limited ACH and SEPA systems, Lightspark provides a global payments infrastructure built on Bitcoin for real-time, low-cost money movement across borders. It connects businesses to a global payments network that supports over 94 countries and 75 currencies.

- Built on Bitcoin: Lightspark’s infrastructure is built on Bitcoin’s open, decentralized foundation, enabling businesses to use native Bitcoin for payments and integrate with the Lightning Network.

- Instant Settlement: The platform offers real-time, instant settlement, allowing money to move 24/7 without the delays common in traditional banking systems.

- Lower fees: By eliminating gatekeepers and hidden charges, Lightspark facilitates payments at a fraction of the cost of legacy systems.

- Cross-border security by default: The network is designed for secure, compliant-ready international payments, integrating robust security protocols for global transfers.

A Modern Infrastructure

For enterprises ready to move beyond legacy payment rails like ACH and SEPA, Lightspark offers a suite of powerful solutions.

- Wallets: A solution for building feature-rich digital wallets with flexible custody, providing real-time access to Bitcoin, Lightning, and stablecoins.

- Digital Banks: A platform for digital banks to connect to a global money network, enabling market expansion and 24/7 payments.

- Exchanges: A solution for cryptocurrency exchanges to connect to the Bitcoin Network, enabling instant transfers and lower operational costs.

- Stablecoins: Tools for creating and distributing stablecoins on the Bitcoin network through Spark, enabling fast and low-cost payment experiences.

As emerging technologies and regulations shape the future of payments, don’t just choose between two outdated options—upgrade to a payment rail built for the internet age. Lightspark enables real-time, low-cost global payments by connecting you to a modern, open network. To see how, learn more or book a demo.